It seems that all we have been doing for the past few months is talking about taxes. The Tax Reform & Job Act did, in fact, give us much to talk about. At one point, it appeared that the bill was going to do away, or significantly reduce, pre-tax savings opportunities currently available to eligible retirement plan participants.

The talk was that after-tax contributions would largely replace pre-tax contributions in 401(k)s, 403(b)s, and other defined contribution plans. In other words, they would have forced everyone into Roth IRA type of arrangements, where you don’t get the near-term incentive of saving on taxes, but the earnings would be tax-free. Fortunately, taxpayers retained the incentives and flexibility to decide for ourselves between pre-tax accounts that defer income taxes or post-tax alternatives that grow tax-free. With both alternatives still available, a common question remains.

Should I do a Roth IRA?

“Should I, or can I, do a Roth IRA?” That is one of the most common discussions I have with clients. The answer can vary, based on several issues.

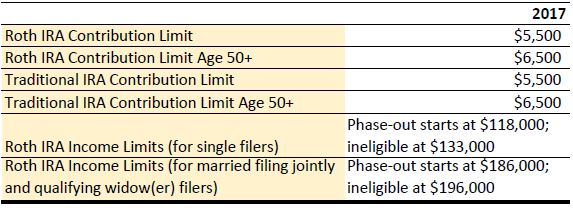

Can you contribute? To contribute to a Roth IRA, your Adjusted Gross Income (AGI) needed to be below $133,000 for 2017, if you are single. For married couples, the AGI limit is $196,000. Some good news is that all those limits increase by $2,000 - $3,000, respectively, for 2018.

Can you convert? Since 2010, there have been no AGI limitations on converting existing IRA balances to Roth IRAs. Even if your income exceeds the AGI limits for contributions, you can convert any traditional IRA amount to a Roth IRA.

Should you convert? This is where it starts getting interesting. If taxes are equal on the front or back end, your result will be the same. Consider if you earned $1,000 and owed 10% tax, you would have $900 to invest. Grow $900 at a hypothetical growth rate, say 7.2%, and it grows to $1,800 in 10 years. In a Roth IRA, that would be tax-free. On the other hand, invest $1,000 pre-tax and it grows to $2,000 at the same 7.2% hypothetical rate, but you would owe $200 (10%) in tax, netting the same $1,800.

So, if you have tax-deferred IRA money you are considering converting to a Roth IRA, the main variable is your future tax rate versus your current one. If you believe your tax rate will be lower today than in the future, than a conversion of pre-tax retirement money may make sense. But, even if you’re not eligible for a deductible Traditional IRA contribution, you are eligible for a non-deductible Traditional IRA contribution, if you have earned income.

Converting non-deductible IRAs that have little or no pre-tax earnings accrued is what is commonly known as a “Back-Door” Roth IRA Contribution. The net effect of contributing after-tax money to a Traditional IRA and converting to Roth IRA is effectively the same as making a contribution.

But, if you have other pre-tax IRAs, it gets more complicated. The IRA Aggregation Rule (IRC Section 408(d)(2)) stipulates that you must treat ALL your IRAs as one account when determining the tax impact of a conversion.

For example, say you have $200,000 of existing pre-tax IRAs and aren’t eligible for a deductible IRA due to your earnings. You decide to make a $5,500 non-deductible Traditional IRA contribution for 2017 and then convert those after-tax dollars to a Roth IRA so that they can grow tax free.

However, due to the IRA Aggregation Rule, you can’t just convert the $5,500 you contributed after-tax. You must first determine what proportion of your IRA is being converted versus the post-tax balance and you must pay tax on the difference.

So, with a $5,500 Roth conversion (IRA funds totaling $200,000 plus the $5,500 contribution equals $205,500), the return-of-after-tax portion will be only 2.68% ($5,500 / $205,500). On this $5,500 Roth conversion, only $147 of after-tax funds will be converted, leaving the other $5,353 of the conversion to be taxed.

To add insult to injury, the burden falls on you to keep records of how much after-tax money remains in your aggregate IRA. This is done on IRS Form 8606, and is required to be updated each year that you have post-tax money in your IRA.

The Back-Door Roth IRA Key

Some good news for those that don’t want to pay taxes today on a Roth IRA conversion is that there are ways to open seemingly closed Back-Door Roth IRAs. The key is to reduce the amount of pre-tax money in your aggregate IRA. Here are a few ways to do that.

Rollover your Traditional IRAs into your 401(k). Most people know that they can rollover retirement balances from previous employer retirement plans into an IRA, but most employer plans accept rollovers from other employer plans, too. Even better, those plans typically also will allow you to rollover any pre-tax IRA money, including Traditional IRAs. The downside can be that your employer plan may have limited investment selection and/or high costs, so some due diligence is required.

For the self-employed, the rollover feature may be a reason to consider a 401(k) for the business instead of other retirement vehicles such as SEP-IRAs or SIMPLE IRAs. The downside here can be that 401(k)s are typically more expensive to administer and have additional tax reporting requirements when they reach a certain size. Businesses that have no employees other than the owner can establish a Solo 401(k), (also known as a Self Employed 401(k) or Individual 401(k)). These plans are designed specifically for employers with no full-time employees other than the business owner and their spouse. Best of all, Solo 401(k)s avoid much of administrative burden and costs of traditional 401(k) plans.

Speaking of spouses! Non-working spouses are eligible to make IRA contributions based on the working partner’s income. In some circumstances, a Back-Door Roth IRA may not make sense for one partner, but it will for the other. A stay-at-home spouse that earns some income from a side business may consider establishing a Solo 401(k) plans for the business. This not only can allow for more pre-tax savings opportunities, but can offer another way into the Back-Door.

Looking for ways to increase your retirement savings and maybe save on taxes now and later? Get in touch.

(If you liked the post, please share. You can also help me keep the lights on by clicking an ad or even buying one of the items listed on the right margin, if it suits you. None of the products appearing in the ads are endorsed by me or ATX Portfolio Advisors.)