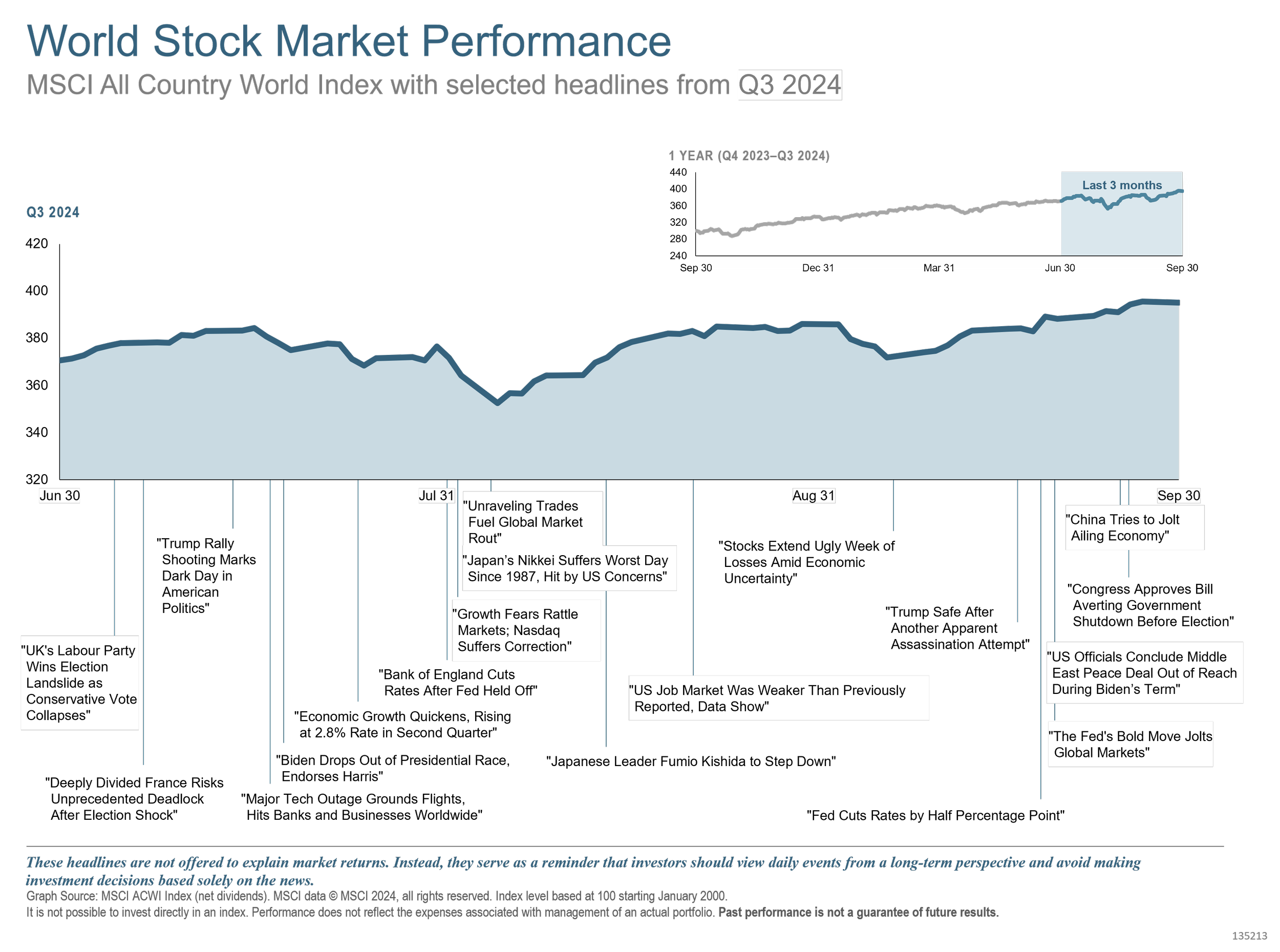

US equities continued to build on a strong start to the year, with many market indices nearing record highs in Q3. However, a rise in volatility, unprecedented since the COVID epidemic, accompanied this increasing momentum. Months of anticipation notwithstanding, the Federal Reserve finally answered the call to lower interest rates in September—a first since 2020—as core inflation showed indications of declining. Although the U.S. markets were robust, developed markets outside of the United States also saw gains. Emerging markets also saw some of the biggest increases in the quarter. On the bond front, U.S. Treasury bonds showed price increases that drove the 10-year yield below 4%.

On September 18, the Fed decided to drop the Federal Funds Rate by half a percentage point to a range of 4.75%–5%. A mixed economic picture and a rising unemployment rate led them to cut by a half-point. Since the upheaval of the market in March 2020, this is the first rate cut we've seen. Inflation reached its lowest point since 2021, with the August core Consumer Price Index showing a 3.2% year-over-year increase—excluding the more erratic food and energy sectors.

Major stock indices fell in two bouts of market weakness, in early August and then in early September. Luckily, both times the markets recovered; the S&P 500 was up 5.53% for the quarter. Not performing as well, the NASDAQ only gained 2.57%. The "Magnificent 7" stocks, including Nvidia, suffered during the August drops; before recovering, their combined market value dropped over $1.3 trillion.

Thanks to huge demand for its chips—which are essential for artificial intelligence applications—Nvidia has been a standout performer this year. With second-quarter earnings of $30 billion in August, the stock had an amazing 121% rise from a year before. But after their most recent quarterly earnings, its stock price dropped—probably because investors had already built in projections of an explosive increase. This reminds us that sometimes high expectations make it more difficult for growth stocks such as Nvidia to keep wowing investors.

Bonds gained for four straight months through August, while U.S. Treasury bonds enjoyed their longest monthly winning run in three years. The 10-year Treasury yield ended Q3 at 3.81%—more than a full percentage point below its current peak in October 2023. The 10-year yield rose above the 2-year, ending the long-standing yield curve inversion. Yields across the curve followed this downward trend for the first time in almost two years.

Globally, value stocks and small caps outperformed growth and large caps. Value stocks topped growth by 3.82%, while small caps surpassed big caps by 2.69%. According to the most recent data through August, high-profitability equities lagged behind their lower-profitability counterparts by 2% in developed countries and 1.4% in developing economies, which is interesting.

Although this hasn't always been the case recently, value stocks have historically beaten growth companies. Between 1927 and 2023, value stocks beat the larger market in 58 of the years, outpacing growth stocks by an average of 4.07% over that time period. In those 58 years where value beat growth, the average difference was 14.83%! Having said that, the present trend certainly doesn’t guarantee future outperformance, but it definitely bears watching.

Looking ahead, the forthcoming U.S. presidential election is another element drawing interest among investors. The late shake-up at the top of the Democratic ticket in the campaign alters the race dynamics and introduces some uncertainty. National polls show a close battle with no obvious frontrunner developing as we get ready for Election Day. Hold your hats, folks; the ride could get bumpy!

Investors naturally feel strongly about the way political events turn out. After all, elections may generate a lot of emotions, and the media most definitely does not hold back on stressing their possible influence. Here is where we might find some solace, though; history has shown that the president is only one of several elements affecting the market over time. Actually, regardless of which party is in charge, stocks have generally gone up over time. Although the temporary commotion of an election can be distracting, we should keep our eyes on long-term objectives and see things from the long run.

In times like these, when passions and opinions may run strong, it helps to step back, inhale deeply, and remind ourselves that a complicated combination of elements shapes markets. One aspect of the puzzle is political leadership; others abound. As Election Day approaches, keep your focus on your goals and remember that good investing is about following your strategy through all kinds of market conditions.

If you have concerns about your current strategy and investments, get in touch to review your plan and portfolio. In the meantime, you can see the slides below for a visual review of Q3 2024.