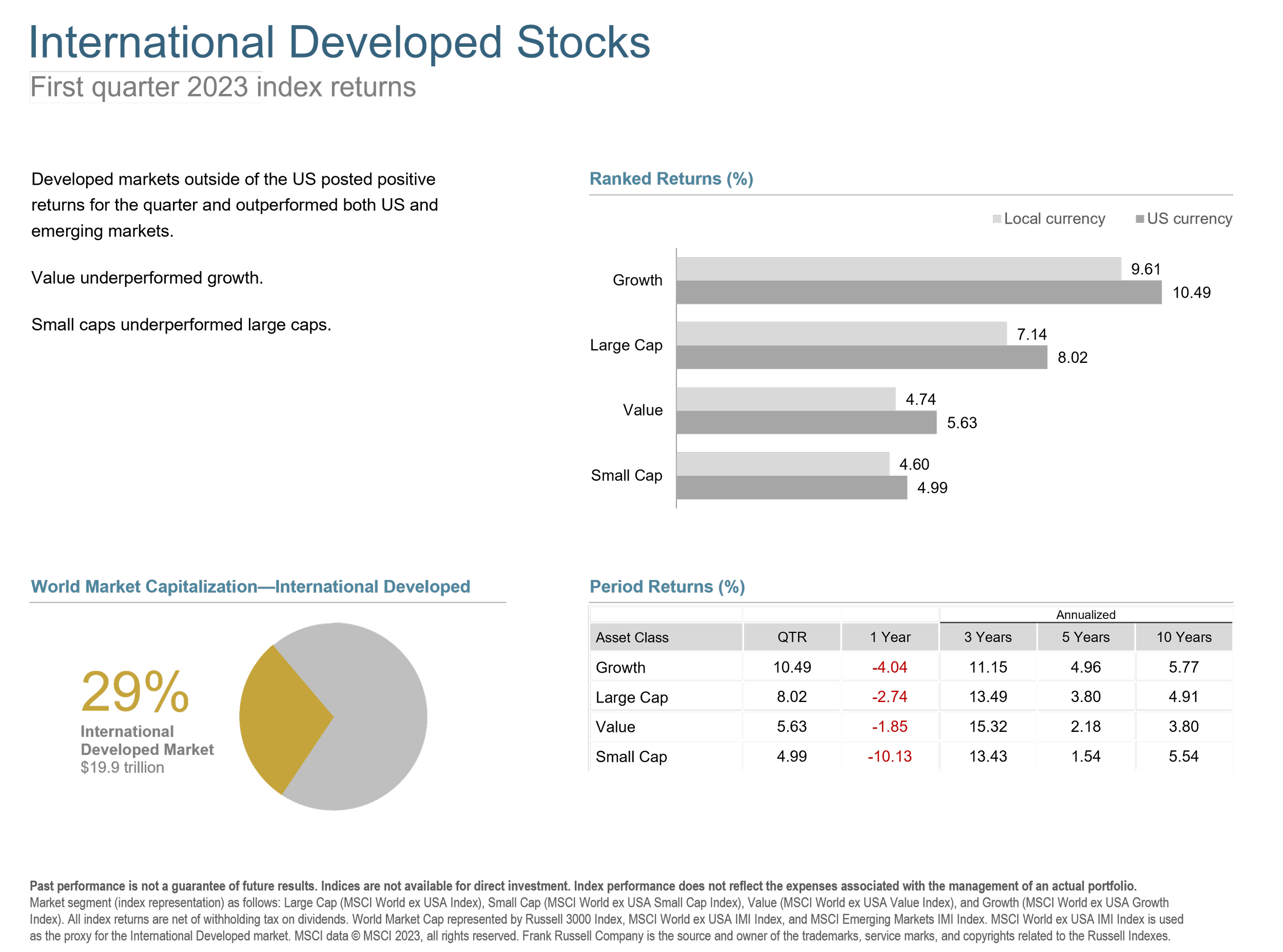

Global stocks were up nearly 7% in Q1, continuing their upward path that began in Q4 of last year. Market volatility was relatively calm until March, when regional bank failures in California and New York suddenly raised concerns about the entire banking sector. Following last year when value stocks beat growth by 20%, the first quarter saw value stocks lag growth by 12%.1

Technology names led the quarter, lifting the returns of large growth stocks. Less profitable growth stocks especially outperformed, with stocks like Nvidia that returned 90%. Energy stocks, many of which were still considered value stocks despite a strong run-up last year, dropped by 3.0%. Financials, hit hard by the previously mentioned banking worries, ended the quarter down 1.8%. Small cap stocks generally underperformed, especially in the US, but not universally. While lower profitability large stocks outperformed, the reverse was true in small caps, where higher profitability stocks generally did better.

In March, the US Consumer Price Index (CPI) fell to 5% year-over-year, marking the 9th consecutive month of retreat from 40 year highs and the lowest level since May 2021. Low unemployment, which perversely has been bad for the market when good numbers are reported, remained strong in March at 3.5%. The tight labor market and persistent inflationary pressures pushed The Fed to raise its key interest rate for the eighth consecutive time, in spite of a possible banking crisis. The Fed also continued their quantitative tightening program but actually grew their balance sheet from $8.3T to $8.7T in March by issuing what amount to emergency loans to banks.

The concerns raised by the runs on Silicon Valley Bank and Signature bank have definitely increased our clients’ anxiety. While there are tactical steps we can take to address some of those concerns (such as keeping our balances at banks below FDIC limits and investing directly in other instruments like US Savings Bonds, Treasury Bills, and money markets), we should always turn to our investment plans to understand the real impact of the risk we are taking. This should help to tune out the noise that current headlines always create and focus on time-tested principles to avoid making shortsighted missteps.

If you would like to review your plan, get in touch. In the meanwhile, you can see the slides below for a review of Q1 2023.

1.As measured by the return of the MSCI All Country World Value IMI Index (net div.) minus the return of the MSCI All Country World Growth IMI Index (net div).