Want a good way to keep your cool the next time one of your kids does something that annoys you? Remember that they will choose your nursing home one day.

In all seriousness, Long Term Care (LTC) planning isn’t a joke. According to a 2015 research brief from the US Department of Health & Human Services, it is estimated that 52% of Americans turning 65 today will develop a disability requiring some form of LTC with an average cost of $138,000.[i] With more than half of us expected to need these types of services, insuring the risk is pretty expensive. If that doesn’t make sense, then a quick review of the principles of insurance may be in order.

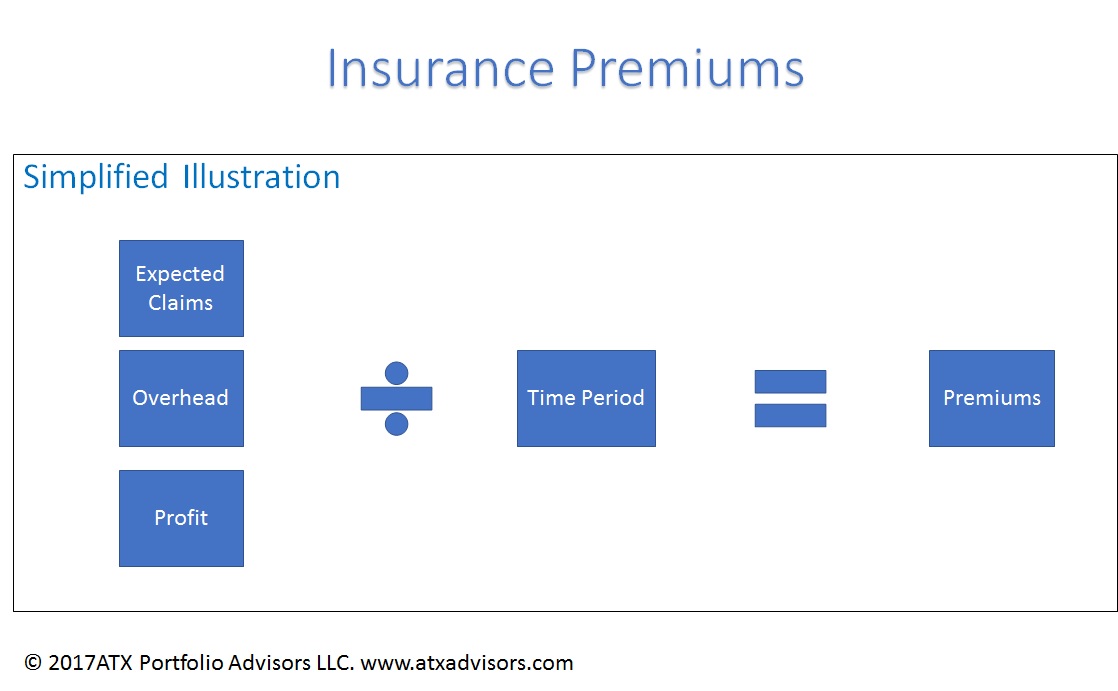

It is important to understand that all insurance is designed, on average, to cost the insured more than will be returned in claims. If that wasn’t the case, every insurance company would go bankrupt. Premiums are a product of expected claims and costs spread over an anticipated timeframe, leaving enough for the insurance company to be profitable.

Thus, low probability high impact events are relatively affordable to insure. Say, for example, you own a $500,000 home in Texas. The risk of a tornado destroying your home is about 1 in 4,101,000.[ii] Even after adding in other low probability events (fire, lightning, etc.), the cost of insurance only winds up being several hundred dollars per year since the insurance company expects to pay out only to a small fraction of their policy holders.

But if the insurance company is expecting to payout $138,000 of claims to 52% their policy holders, the premiums will be much higher. In a nutshell, this is why LTC insurance is so expensive. It also means that you should include LTC planning in your financial plan and understand the different ways to deal with it.

Have Medicaid pay for it

Some readers may think I meant to say Medicare, but Part A covers only up to 100 days of “skilled nursing” care facility per illness. If the need for care is custodial (not related to a specific illness episode), then there is no LTC coverage from Medicare. To qualify for Medicaid in Texas this year, you must either be disabled or 65 years old and have annual household income below $23,879 for an individual or $32,155 for a couple. Assets are limited to $2,000 for an individual or $3,000 for a couple, but you are allowed to retain your home, vehicles, limited burial funds, personal belongings, and some types of life insurance.

This may sound like a plan of last resort, and for many it is, but 60% of nursing home residents are currently being paid by Medicaid[iii].

Buy LTC Insurance

Even though it can be expensive, for some people, it will make sense to buy LTC insurance. The policies typically only cover up to certain amounts for specific time periods once an elimination period has elapsed (usually 90 days). For example, I shopped quotes among several popular carriers for a hypothetical 60-year-old male with a $200 per day benefit that lasts for 5 years after a 90-day elimination period, plus a 3% compound inflation rider.

Annual premiums averaged about $3,750 per year (and aren’t fixed). The premiums are tax deductible, along with other unreimbursed medical expenses, to the extent that they exceed 10% of adjusted gross income. The maximum the policy would pay out in today’s dollars is about $347,000, if the benefit was collected for 5 years minus the first 90 days (about 1735 days, not counting the leap year(s)).

For someone with a modest nest egg, this insurance may make sense. Say you anticipate having $500,000 at retirement that will generate about $20,000 (4%) per year of income. A significant stay in a LTC facility could be devastating to the nest egg because the principal would erode and the amount of income generated would drop, leading to faster principal erosion. Spending 20% if that income to avoid the need to go on Medicaid and leave heirs nothing may be a very reasonable choice.

Self Fund

For someone that has a larger amount of resources, the prospect of self-funding a LTC goal may be attractive. Given the probability of needing LTC at some point, the case can be made that insuring the risk is essentially a pre-payment plan anyway.

When you add in the reality that the average nursing home stay is just over one year[iv], it can be attractive for many to pay themselves instead of an insurance company. My preference for doing this type of planning is to add a LTC expense beginning today into a financial plan and run a stochastic model to understand if that expense would have a material effect on the plan. If we can show that the odds of success remain relatively high, it can make the decision to self-insure easier.

Conclusion

Finally, there is an emotional element to any insurance discussion. Some people can’t sleep at night without knowing they are fully covered while others can’t stand the thought of sending a dime to an insurer. As a fee-only financial advisor that doesn’t sell any product for commissions or other incentives, we not only can help you determine the right strategy for you and your family, we can also help you with your due diligence if you are in the market for a solution.

If you would like to discuss your plan, get in touch.

[i] https://aspe.hhs.gov/basic-report/long-term-services-and-supports-older-americans-risks-and-financing-research-brief

[ii] https://www.accuweather.com/en/weather-blogs/weathermatrix/odds-of-bad-weather-vs-winning-powerball/2100929

[iii] https://www.kff.org/infographic/medicaids-role-in-nursing-home-care/

[iv] http://www.nber.org/chapters/c12970