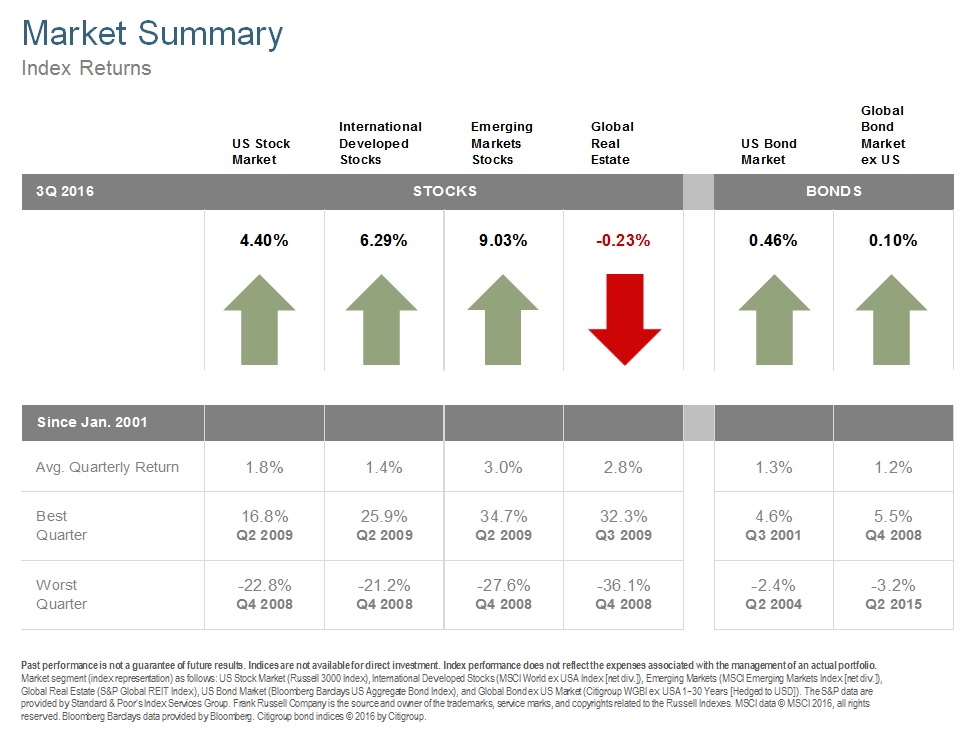

Despite the uncertainty created by the still tight presidential election, stocks and bonds generally had positive returns for the quarter, with the Dow, S&P 500, and NASDAQ all setting record highs. As the quarter was coming to a close, the omnipresent question of when, or if, central banks will end their "do no harm" mode in favor of raising rates here in the US or continuing to ease them in Europe and Japan led to some volatility.

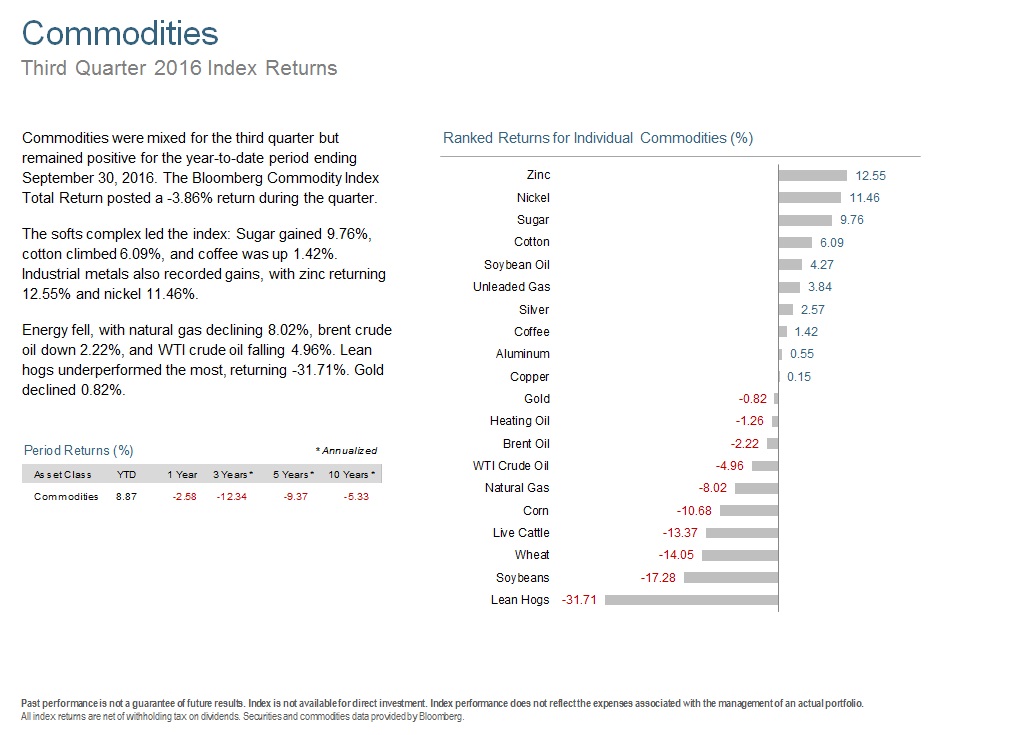

Small cap stocks were the best performing asset class, which usually bodes well for economic growth. Not surprisingly, REITs, which should be sensitive to rising rates, were weaker during the quarter. However, commodities, which you may expect to rise with inflation expectations, were mixed.

As has been the case over the past few years, the guessing game of trying to differentiate temporary reversion to the mean against longer term trends proved to be anyone’s guess. This is why I avoid “tactical” approaches to investing for long term goals, because it is essentially making a guess.

Historically, there are more up days in the stock market than down days. There are also more up months versus down months and more up years versus down years. Betting against the house is a losing proposition. Worse, even if you guess correctly on a short term drop, you have to guess again on the reversal in order to profit.

Just as the odds of the ball landing on red don’t change even if it landed on black each of the last dozen spins, the last eight months of positive returns don’t increase the odds that next month will be down. Be thankful for the string of positive returns and when we see the next downturn, remain steadfast in the knowledge that the odds favor staying the course.

Now, for the Q3 2016 Market Review...